The RBI has updated its rules on how banks handle savings and term deposit accounts for minors. Now, any minor (through a guardian) can open an account, and children aged 10+ can independently operate savings/term deposits under bank-defined limits. The circular aims to unify old policies, improve inclusion (especially for mothers as guardians), and set a July 1, 2025 deadline for compliance.

Why This Circular Changes the Game for Minor Banking

Minors often hold bank accounts for school scholarships, pocket money, or early savings habits. But until now, the rules governing these accounts were scattered across multiple RBI circulars, creating operational confusion for banks and fintechs.

More importantly, there was ambiguity around allowing mothers to act as legal guardians for minor accounts, especially in communities where laws favoured paternal guardianship. This posed hurdles for financial inclusion, especially for single mothers or women seeking financial autonomy for their children.

With this April 2025 circular, RBI consolidates and simplifies the guidelines, making it easier and safer for minors to open and operate bank accounts.

Key Highlights

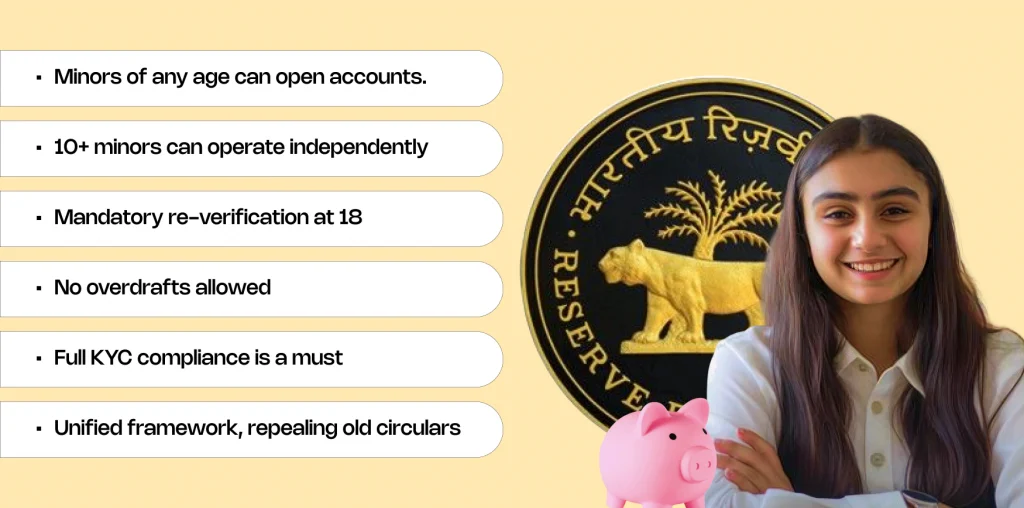

- Minors of any age can open accounts – but only through their natural or legal guardians (including mothers). This affirms a key step toward gender-neutral guardianship in banking.

- 10+ minors can operate independently – Banks may, as per their risk policy, allow minors aged 10 and above to manage savings or term deposits on their own, including setting limits on amounts and transactions. Think of this like a “financial learner’s license”-banks decide the training wheels.

- Mandatory re-verification at 18 – When the minor turns major (i.e., 18), banks must:

- Get fresh operating instructions

- Collect a specimen signature

- Confirm balances if a guardian operated the account

- Communicate the changeover well in advance

- Get fresh operating instructions

- Extra facilities allowed (with caution) – Banks may extend internet banking, ATM/debit cards, and cheque books to minor accounts based on:

- Risk management frameworks

- Customer suitability

- Product appropriateness

- Risk management frameworks

- No overdrafts allowed – Minor accounts must always maintain a positive balance. This ensures legal and contractual protection, given minors can’t legally be bound by debts.

- Full KYC compliance is a must – Customer Due Diligence (CDD) and Ongoing Due Diligence must align with the Master KYC Direction, 2016, ensuring minor accounts are not used for fraud or money laundering.

- Unified framework, repealing old circulars – RBI repealed 10 earlier circulars dating back to 1976. Now there’s a single source of truth for handling minor accounts.

Impact on Fintechs

This is more than a compliance update-it’s an opportunity for fintechs building financial products for the youth segment.

What startups should do now

- Update your minor account flows

- Ensure eligibility checks for guardians

- Embed logic for age-based access to features like UPI, cards, and netbanking

- Ensure eligibility checks for guardians

- Plan for 18+ transitions

- Automate birthday-based triggers

- Build UI/UX to nudge users for KYC refresh, signature collection, and balance confirmation

- Consider gamified reminders (“Time to graduate your account!”)

- Automate birthday-based triggers

- Revisit risk models

- If you’re a neo-bank or payment bank offering minor accounts, revise your internal limits for 10+ age groups (e.g., max balance, daily transfer cap)

- If you’re a neo-bank or payment bank offering minor accounts, revise your internal limits for 10+ age groups (e.g., max balance, daily transfer cap)

- Guardian-based flows

- Ensure systems allow for the mother as the sole guardian

- Adjust legal documentation and consent protocols accordingly

- Ensure systems allow for the mother as the sole guardian

- Data and KYC compliance

- Refresh your onboarding checks to align with updated KYC norms for minors

- Monitor minor accounts to ensure they’re not misused (e.g., mule accounts)

- Refresh your onboarding checks to align with updated KYC norms for minors

- Communicate clearly with users

- Add FAQs for parents/guardians

- Clarify how balances, operations, and upgrades work once the child turns 18

- Add FAQs for parents/guardians

Product, Engineering, and Legal teams should:

- Product: Define access levels for minors, account tiers, and parental controls

- Engineering: Add age-based restrictions in backend services/APIs

- Legal/Compliance: Update account opening documentation and internal policy manuals

Deadline

All banks (and by extension, fintechs operating under partnerships) must align their systems and policies to the new circular by July 1, 2025. Till then, existing policies can continue.

Digging Deeper: Why This Matters Now

The timing of this RBI move is strategic. With digital banking rapidly penetrating Tier 2 and 3 cities-and children as young as 10 using UPI, prepaid wallets, and gamified savings apps-the financial system needs a strong but flexible framework to govern these interactions.

Let’s not forget the massive rise in youth-focused fintech products. From “first bank account” platforms like Junio and Fyp to prepaid card startups like Akudo or FamPay, there’s a whole ecosystem targeting minors. But so far, many of these solutions operated on prepaid license workarounds, often without integrating directly with deposit accounts.

RBI is now making it easier for these platforms to formally partner with banks and offer real savings accounts to minors with age-appropriate controls. This bridges the gap between play-money and real-money banking.

A Closer Look at Guardian Flexibility

A standout feature of the new circular is its explicit inclusion of mothers as legal guardians, even if the father is alive. This seemingly small change has big implications:

- Earlier, banks hesitated to open accounts with only the mother as guardian, citing the Hindu Minority and Guardianship Act.

- Now, the RBI confirms that savings/term accounts do not legally conflict with personal laws, as long as there’s no overdraft or debt created.

- This aligns with modern family structures-single mothers, shared custody, or fathers unavailable due to migration or work.

For fintechs offering family finance tools (like “family accounts” or “parent-child budget planners”), this is crucial. You can now confidently build flows where either parent, especially the mother, can be the account initiator.

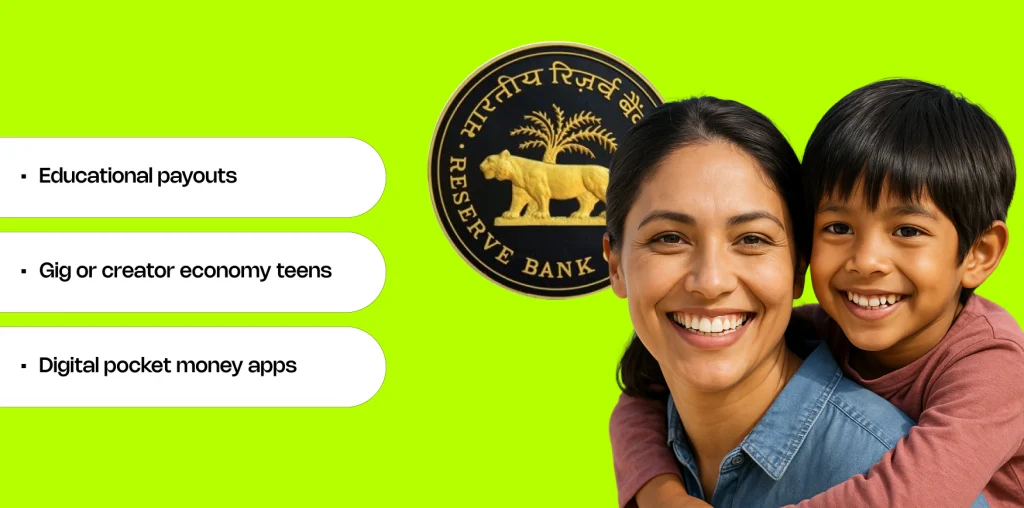

What Minors Can Do with Their Bank Accounts

Minors aged 10+ can now have full operational control if the bank permits it. This opens a range of use cases:

- Educational payouts – Students receiving scholarships or tuition reimbursements can access accounts directly.

- Gig or creator economy teens – Young YouTubers, coders, or content creators can receive earnings into bank accounts in their own names.

- Digital pocket money apps – Parents can transfer funds to kids’ accounts while retaining oversight.

In each case, fintechs must ensure clear communication and usage limits, such as:

- Daily transaction caps (e.g., ₹2,000/day)

- No international transfers

- No high-risk instruments (like loans or investments)

What About Tax, Nominee, and Legal Implications?

Though not directly addressed in the circular, here are some points fintech legal teams should track:

- Tax Filing – Income in a minor’s name may still be clubbed with the guardian’s under the Income Tax Act. Design app flows accordingly.

- Nominee Setup – Minor accounts can have nominees, but fintechs must include UI flows to manage this.

- Legal Protections – Since minors can’t contract debt, no minor account should be linked to credit products like overdrafts or BNPL.

Conclusion

The RBI’s circular may seem procedural, but it opens the doors to a more inclusive, structured, and digital-friendly financial experience for India’s next generation. Fintechs targeting teens, parents, and students now have a cleaner regulatory slate to build trust-based products.

This also signals a clear shift by RBI: balancing risk with access – even for the youngest of customers.

Need help updating your minor account policies? Talk to BeFiSc – we help fintechs stay compliant, confidently.

FAQs

Can a minor open a bank account without a parent or guardian?

No. A minor can open a savings or term deposit account only through a natural or legal guardian. However, the RBI has clarified that mothers are equally recognised as guardians, even if the father is alive.

Can minors aged 10 and above operate bank accounts independently?

Yes, minors aged 10+ may be allowed to operate their savings or term deposit accounts independently, subject to limits defined by the bank’s risk policy. Banks can set caps on balances, withdrawals, and transaction types.

Are debit cards, internet banking, or cheque books allowed for minor accounts?

Yes, banks may offer these facilities based on their internal risk framework, customer suitability, and product appropriateness. However, overdrafts or negative balances are strictly not permitted on minor accounts.

Is full KYC required for minor bank accounts?

Yes. All minor accounts must comply with RBI’s KYC and ongoing due diligence norms, ensuring they are not misused for fraud, mule activity, or money laundering.